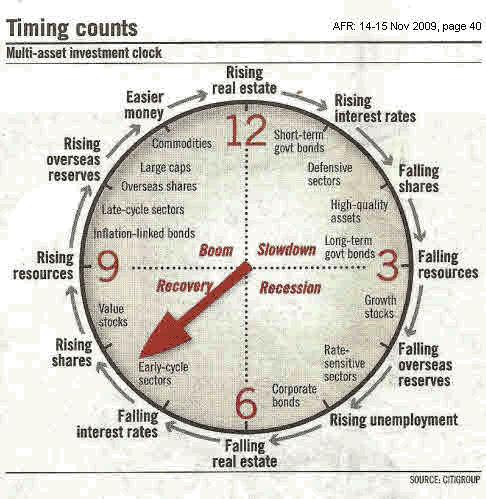

The Investment Clock: Revisited

There are numerous variations to the age old “investment clock”. Citigroup’s version below is the most relevant to our market that I can find.

There was a time when I entered the market many moons ago as a starry eyed analyst, that you could “almost” set your watch to the clock. This was a world where Europe and the US were, from an economic point of view, the world. You could only sell stock you owned. Humans operated the market and an order of 10 shares was considered an unmarketable parcel.

The world was a lot simpler, more transparent and successful investing depended on one’s ability to analyse a company and the macro issues of the industry within which the said company operated. Today there are so many extraneous factors which affect a given share price, that it really is akin to negotiating your way through a minefield, often blindfolded.

I’m still trying tomake up my mind whether the clock’s gone haywire and there is a total disconnect between the traditional relationships within the clock; whether the clock appears to be permanently stuck between 3 and 7 o’clock; or whether there is some other more insidious factor at play here that is distorting the clock.

I suspect it’s the latter.

The greatest single change that has affected the market over the past 10 years is the phenomenal growth of China which has gone from an economic backwater to the world’s 2nd largest economy. But what has been the most destabilising aspect of this growth is that China has single handedly redefined the commodity complex. There are few major commodities where China isn’t the largest consumer. This has effectively changed the whole balance of power in sea-borne trade, away from those that had dictated terms for the previous 50 years.

While China has been building itself into the next world superpower, serious cracks have emerged in those economies that had been, up until the GFC, ” the world” – Europe, the US, and Japan. So we’ve effectively had these two powers working in opposite directions to each other and Australia has been caught in the middle.

There couldn’t possibly be a more schizophrenic market for Australia to operate in. On one hand, the US market, which has traditionally always dictated which direction our own moves in, has fallen an unprecedented amount; and then recovered. On the other, China, our single largest customer, held the world together during the tough times; but now panic has set in as the world is debating whether the party is over.

So, probably for the first time in history, we’ve had these two opposing forces at almost perfectly opposite positions on the “investment clock”; and we’re stuck in the middle, not quite knowing which direction to go.

Right now the US market appears to be trading at 8 o’clock while the Doom Brigade would have us believe that China is trading at 1 o’clock. The Australian market is torn in the middle. Our investment clock appears to have grown into some grotesque Frankensteinian creation with multiple hands. And, through this, we are supposed to gain some guidance from the clock as to where we are currently and where we are going.

What I am trying to demonstrate, in a very roundabout way, is that investing in the current climate in Australia has possibly never been more difficult. With one eye on Chinese production data (which we may or may not be able to rely on) and the other on the supposedly improving US economy, the signals are very confusing indeed.

Those investing in the Australian resource sector appear to have gotten to the point where they’ve just thrown all the cards in the air and walked away. We are now at a point not dissimilar to that following the collapse of Lehman Brothers, when we were all convinced that the world as we knew it was going to cease to exist. One of the most poignant examples of complete capitulation at that time was the sell down of Giralia, which had been one of the market darlings. Giralia were sold from $2.80 down to 35 cents. Everyone I spoke to at the time believed that they were about to implode, even thought they had $25 million in the bank at the time. Giralia continued to beaver away doing what they were doing and, 18 months later, were taken over at $5.50.

As we speak the Australian Small Cap Resource sector is at a 12 month low. From these levels there will be numerous Giralia examples which we’ll talk about when the recovery finally comes. But no one can predict when that point will come. I do know, though, that there are many examples of grossly oversold positions out there and those that are prepared to be patient can begin to nibble away.

You don’t need to go too far down the food chain to find very good value. Look for those companies with plenty of cash to see them through the long cold winter. Look for high grade, low operating cost operations. Look for a grade locations in sound geopolitical locations. And wait.